Financial Fitness Test

Do you have a strong financial why and a measurable deadline?

Whatever your motivation, you have until the 5th April to make use of available personal tax allowances. Continue reading

Financial Fitness Test

Do you have a strong financial why and a measurable deadline?

Whatever your motivation, you have until the 5th April to make use of available personal tax allowances. Continue reading

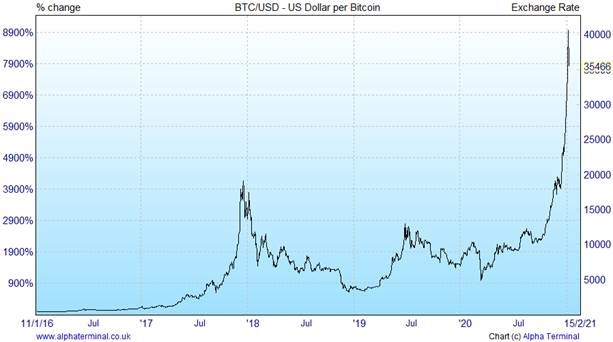

It is less than a year since Rishi Sunak presented his first Budget, after having been in the role of Chancellor for less than a month. His despatch box première featured an allocation of £12bn towards mitigating the impact of the Covid-19. Ironically, on the same day as Mr Sunak revealed that boost to spending, the World Health Organisation declared the outbreak a pandemic. Total expenditure in the U.K. on dealing with the pandemic is now estimated to be around £300bn.

![]()

The valuation of everything

Page 1 of the investing textbook states one should only take risk when one is being rewarded for doing so. This means that the valuation of everything is based off the expected return of the lowest risk asset. It is widely accepted that the lowest risk investment asset available is long dated government bonds. The proxy for this is the 10 year UK government bond in the UK and the 10 year treasury in the USA.Continue reading

Budget winners and losers

Yesterday Rishi Sunak delivered a budget to guide us out of the Covid crisis. We all knew that the extraordinary schemes to prop up an economy that had the ‘pause’ button pressed on it would carry a large long term cost.Continue reading

From a northern hemisphere perspective, Spring 2021 formally begins on Saturday 20 March however – for both recent weather and economic watchers – February showed some real progress that boosted signs of optimism for the rest of the year.

![]()

The first month of a new year ended as a disappointment for the average U.K. investor, especially as a contrast to the widespread excitable returns seen in the last two months of 2020. However, the month of January alone rarely gives us every answer and the unique nature of both the U.K. market alone and collectively the entire world has a wide range of potential outcomes.

![]()

We wish you a safe, healthy, and prosperous New Year! These words are even more meaningful given the most deadly and economically crippling ‘Black Swan’ event that we have experienced in the last century—COVID-19. After unprecedented fiscal and monetary stimulus, the record-setting development of multiple effective vaccines has elevated optimism that we will experience the ‘thrill of victory’ over this nemesis in the upcoming year.

![]()

Yesterday evening we got the results of the Georgia runoff elections. The Democrats won both of the seats which means the Senate will have a 50-50 partisan split with incoming vice-president Kamala Harris having the tiebreaking vote. We would expect her to vote Democrat!

It means that Joe Biden and the Democrats have a much better chance of getting through legislation and making changes to both corporate America and Main Street. Some popular Democrat policies include higher tax rates to fund more government spending, climate-friendly initiatives and increased regulation of the technology titans and pharmaceutical sectors.

A big rally across global equity markets. The UK market hit its highest level since March. The biggest winners were those sectors which have been largely out of favour such as banks, oil and gas and mining. In general, any sectors that will benefit from increased inflation and higher interest rates led the market higher. This is the so-called ‘reflation trade’. These are also areas where investor positioning is generally underweight so as we have experienced before rotations often have a large magnitude and are swift. Previously these rotations have not had much-staying power.

The margins are still very thin in terms of majorities in both House and the Senate so whilst the Democrats will have more scope to shape policy and get its chosen nominees confirmed, the usual checks and balances should mean now is not the time to completely rip up the playbook and start over!

The value of investments, and the income derived from them, can fall as well as rise. You may get back less than invested. Past performance is not a reliable guide to future returns.